M11 應用逕向基底函數網路於股票預測 (Stock Market Prediction Using Radial Basis Function Network)

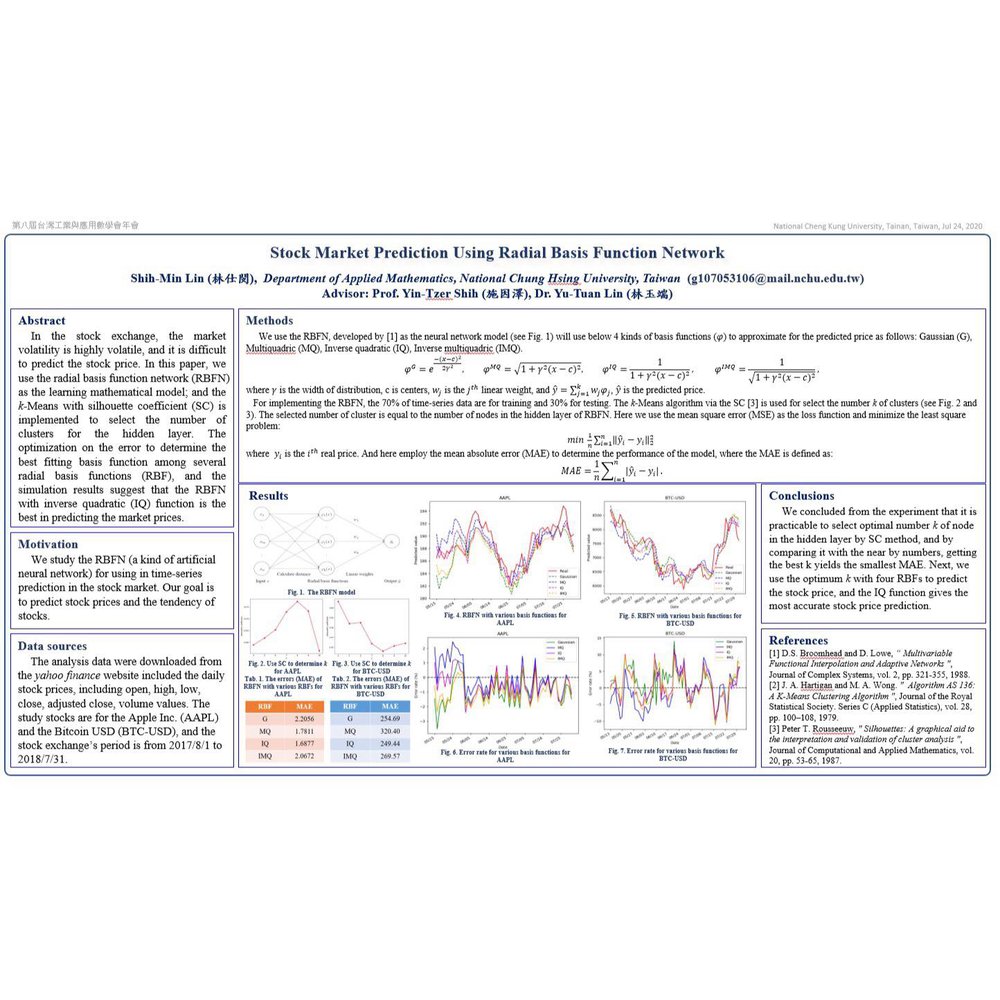

In the stock exchange, the market volatility is highly volatile, and it is difficult to predict the stock price. In this paper, we use the radial basis function network (RBFN) as the learning mathematical model; and the k-Means with silhouette coefficient (SC) is implemented to select the number of clusters for the hidden layer. The optimization on the error to determine the best fitting basis function among several radial basis functions (RBF), and the simulation results suggest that the RBFN with inverse quadratic (IQ) function is the best in predicting the market prices.